Why Airbnb Stock Isn’t The Best Travel Recovery Play

UKRAINE – 2021/03/10: In this photo illustration, an Airbnb logo seen displayed on a smartphone and … [+]

Airbnb (NASDAQ: ABNB) stock is down by close to 15% from its all-time highs, trading at about $188 per share, due to the broader sell-off in high-growth technology stocks. However, the outlook for Airbnb’s business is actually very strong. It seems reasonably clear that the worst of the pandemic is now behind us and there is likely to be considerable pent-up demand for travel. Covid-19 vaccination rates in the U.S. have been trending higher, with around 30% of the population having received at least one shot, per the Bloomberg vaccine tracker. Covid-19 cases are also well off their highs. Now, Airbnb could have an edge over hotels, as people opt for less densely populated locations while planning longer-term stays. Airbnb’s revenues are likely to grow by about 40% this year, per consensus estimates. In comparison, Airbnb’s revenue was down only 30% in 2020.

While we think that the long-term outlook for Airbnb is compelling, given the company’s strong growth rates and the fact that its brand is synonymous with vacation rentals, the stock is expensive in our view. Even post the recent correction, the company is valued at over $113 billion, or about 24x consensus 2021 revenues. Airbnb’s sales are likely to grow by about 40% this year and by about 35% next year, per consensus estimates. There are much cheaper ways to play the recovery in the travel industry post-Covid. For example, online travel major Expedia which also owns Vrbo, a fast-growing vacation rental business, is valued at about $25 billion, or just about 3.3x projected 2021 revenue. Expedia growth is actually likely to be stronger than Airbnb’s, with revenue poised to expand by 45% in 2021 and by another 40% in 2022 per consensus estimates.

See our interactive dashboard analysis on Airbnb’s Valuation: Expensive Or Cheap? We break down the company’s revenues and current valuation and compare it with other players in the hotels and online travel space.

[2/12/2021] Is Airbnb’s Rally Justified?

Airbnb (NASDAQ: ABNB) stock has rallied by almost 55% since the beginning of 2021 and currently trades at levels of about $216 per share. The stock is up a solid 3x since its IPO in early December 2020. Although there hasn’t been news from the company to warrant gains of this magnitude, there are a couple of other trends that likely helped to push the stock higher. Firstly, sell-side coverage increased considerably in January, as the quiet period for analysts at banks that underwrote Airbnb’s IPO ended. Over 25 analysts now cover the stock, up from just a couple in December. Although analyst opinion has been mixed, it nevertheless has likely helped increase visibility and drive volumes for Airbnb. Secondly, the Covid-19 vaccine rollout is gathering momentum in the U.S., with upwards of 1.5 million doses being administered per day, and Covid-19 cases in the U.S. are also on the downtrend. This should help the travel industry eventually get back to normal, with companies such as Airbnb seeing significant pent-up demand.

That being said, we don’t think Airbnb’s current valuation is justified. (Related: Airbnb’s Valuation: Expensive Or Cheap?) The company is valued at about $130 billion, or about 31x consensus 2021 revenues. Airbnb’s sales are likely to grow by about 37% this year. In comparison, online travel giant Expedia which also owns Vrbo, a growing vacation rental business, is valued at about $20 billion, or just about 3x projected 2021 revenue. Expedia is likely to grow revenue by over 50% in 2021 and by around 35% in 2022, as its business recovers from the Covid-19 slump.

[12/29/2020] Pick Airbnb Over DoorDash

Earlier this month, online vacation platform Airbnb (NASDAQ

Covid-19 Helps DoorDash’s Numbers, Hurts Airbnb

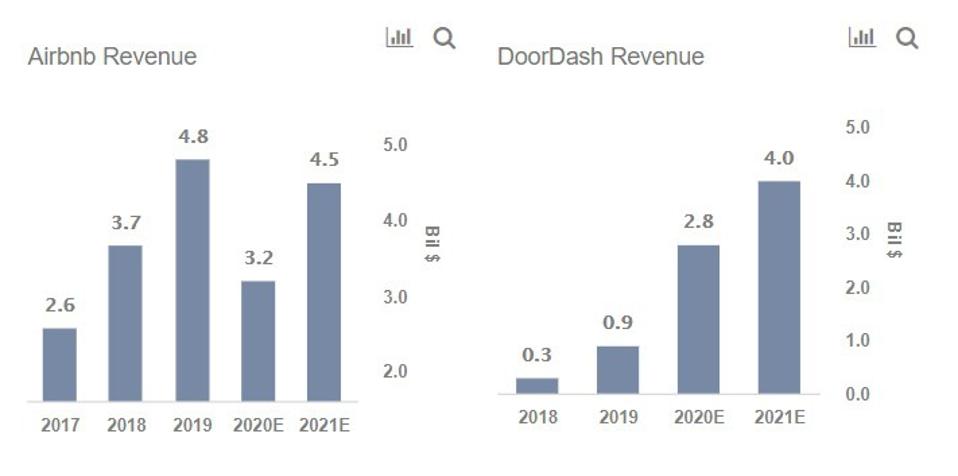

Both Airbnb and DoorDash are essentially technology platforms that connect buyers and sellers of vacation rentals and food, respectively. Looking purely at the fundamentals in recent years, DoorDash looks like the more promising bet. While Airbnb trades at about 20x projected 2021 Revenue, DoorDash trades at just about 12.5x. DoorDash’s growth has also been stronger, with Revenue growth averaging about 200% per year between 2018 and 2020 as demand for takeout soared through the Covid-19 pandemic. Airbnb grew Revenue at an average rate of about 40% prior to the pandemic, with Revenue likely to drop this year and recover to close to 2019 levels in 2021. DoorDash is also likely to post positive Operating Margins this year (about 8%), as costs grow more slowly compared to its surging Revenues. While Airbnb’s Operating Margins stood at around break-even levels over the last two years, they will turn negative this year.

Revenue

The Airbnb Story Still Has Appeal

However, we think the Airbnb story has more appeal compared to DoorDash, for a couple of reasons. Firstly in the near-term, Airbnb stands to gain considerably from the end of Covid-19 with highly effective vaccines already being rolled out. Vacation rentals should rebound nicely, and the company’s margins should also benefit from the recent cost reductions that it made through the pandemic. DoorDash, on the other hand, is likely to see growth moderate considerably, as people start returning to dine in restaurants.

There are a couple of long-term factors as well. Airbnb’s platform scales much more easily into new markets, with the company’s operating in about 220 countries compared to DoorDash, which is a logistics-based business that has thus far been restricted to the U.S alone. While DoorDash has grown to become the largest food delivery player in the U.S., with about 50% share, the competition is intense and players compete primarily on cost. While the barriers to entry to the vacation rental space are also low, Airbnb has significant brand recognition, with the company’s name becoming synonymous with rental holiday homes. Moreover, most hosts also have their listings unique to Airbnb. While rivals such as Expedia are looking to make inroads into the market, they have much lower visibility compared to Airbnb.

Overall, while DoorDash’s financial metrics currently appear stronger, with its valuation also appearing slightly more attractive, things could change post-Covid. Considering this, we believe that Airbnb might be the better bet for long-term investors.

[12/16/2020] Making Sense Of Airbnb Stock’s $75 Billion Valuation

Airbnb (NASDAQ: ABNB), the online vacation rental marketplace, went public last week, with its stock almost doubling from its IPO price of $68 to about $125 currently. This puts the company’s valuation at about $75 billion as of Tuesday. That’s more than Marriott – the largest hotel chain – and Hilton hotels combined. Does Airbnb – which has yet to turn a profit – justify such a valuation? In this analysis, we take a brief look at Airbnb’s business model, and how its Revenues and growth are trending. See our interactive dashboard analysis for more details. In our interactive dashboard analysis on on Airbnb’s Valuation: Expensive Or Cheap? we break down the company’s revenues and current valuation and compare it with other players in the hotels and online travel space. Parts of the analysis are summarized below.

How Have Airbnb’s Revenues Trended In Recent Years?

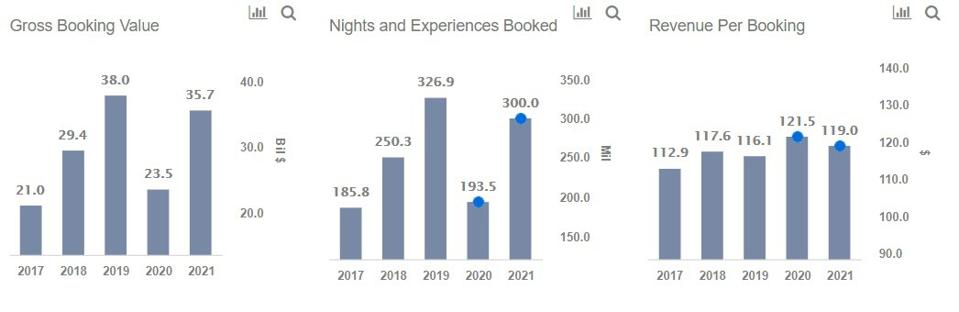

Airbnb’s business model is simple. The company’s platform connects people who want to rent out their homes or spare rooms with people who are looking for accommodations and makes money primarily by charging the guest as well as the host involved in the booking a separate service fee. The number of Nights and Experiences Booked on Airbnb’s platform has risen from 186 million in 2017 to 327 million in 2019, with Gross Bookings soaring from around $21 billion in 2017 to about $38 billion in 2019. The portion of Gross Bookings that Airbnb recognizes as Revenue rose from $2.6 billion in 2017 to around $4.8 billion in 2019. However, the number is likely to fall sharply in 2020 as Covid-19 has hurt the vacation rental market, with total Revenue likely to fall by about 30% year-over-year. Yet, with vaccines being rolled out in developed markets, things are likely to start returning to normal from 2021. Airbnb’s large inventory and affordable prices should ensure that demand rebounds sharply. We project that Revenues could stand at about $4.5 billion in 2021.

Revenue

Making Sense Of Airbnb’s $80 Billion Valuation

Airbnb was valued at about $75 billion as of Tuesday’s close, translating into a P/S multiple of about 16.5x our projected 2021 Revenues for the company. For perspective, Booking Holdings – among the most profitable online travel agents – traded at about 6x Revenue in 2019, while Expedia traded at 1.3x and Marriott – the largest hotel chain – was valued at about 2.4x sales prior to the pandemic. Moreover, Airbnb remains deeply loss-making, with Operating Margins standing at -16% in 2019, versus 35% for Booking and 7.5% for Expedia. However, the Airbnb story still has appeal.

Firstly, growth has been, and is likely to remain, strong. Airbnb’s Revenue has grown at over 40% each year over the last 3 years, compared to levels of about 12% for Expedia and Booking Holdings. Although Covid-19 has hit the company hard this year, Airbnb should continue to grow at high double-digit growth rates in the coming years as well. The company estimates its total addressable market at about $3.4 trillion, including $1.8 trillion for short-term stays, $210 billion for long-term stays, and $1.4 trillion for experiences.

Secondly, Airbnb’s asset-light model should also help its profitability in the long-run. While the company’s variable costs stood at about 25% of Revenue in 2019 (for a 75% gross margin) fixed operating costs such as Sales and marketing (about 34% of Revenues) and product development (20% of Revenue) currently remain high. As Revenues continue to grow post-Covid, fixed cost absorption should improve, helping profitability. Moreover, the company has also trimmed its cost base through Covid-19, as it laid off about a quarter of its staff and shed non-core operations and it’s possible that combined with the possibility of a strong Recovery in 2021, profits should look up.

That said, a 16.5x forward Revenue multiple is high for a company in the online travel business. And there are risks including potential regulatory hurdles in large markets and adverse events in properties booked via its platform. Competition is also mounting. While Airbnb’s brand is strong and generally synonymous with short-term residential rentals, the barriers to entry in the space aren’t too high, with the likes of Booking.com and Agoda launching their own vacation rental platforms. Considering its high valuation and risks, we think Airbnb will need to execute very well to simply justify its current valuation, let alone drive further returns.

Want exposure to the increasing digitization of the economy through and post Covid-19? Check out our theme on Internet Infrastructure Stocks

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams